- home

- Sustainability / ESG Information

- Social

- Add value through DX

Mebuki Financial Group is advancing various initiatives toward transformation using digital technology to aim for sustainable growth and strengthened competitiveness. As specific results of DX, we are realizing improvements in customer service, efficiency in internal operations, and faster management decision-making. Through these initiatives, we will promote our own growth and establish a solid position, while contributing to the digital transformation of the entire region by returning our experience, know-how, and corporate connections to the local community.

Measures under 4th MTGBP

Strategic utilization of generated AI and machine learning

Enhancement of personalized marketing through the utilization of AI with internal data, sharing of know-how within the Group, etc.

Upgrading offensive DX and defensive DX

Expansion of tablet functions at our branches, introduction of digital channels for corporate customers, and reform of corporate internet banking

Developing human resources for DX

Development of DX human resources suited to actual business conditions and improving the levels of expertise of DX leaders among human resources

Infrastructure development for supporting DX

Renovation of groupware, CRM, and SFA, and improvements to communications and device environments

Enhancing consulting services with human-driven value

Digital contact points with UI/UX friendliness

Efficient and smart office work Improving Productivity through Strategic Use of Data and AI

Strategic utilization of data and AI to improve productivity

High-value-added Channels and Improving Convenience

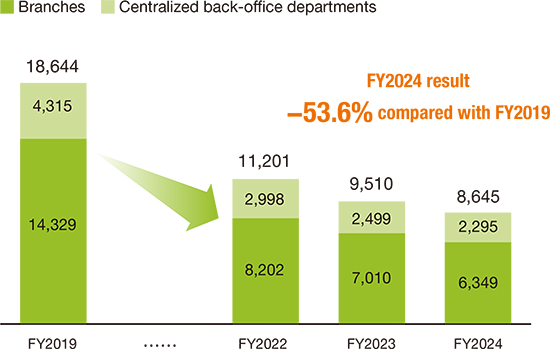

Transformation of Branches to be “Workless”

To share a common definition and understanding of the term DX as the Group, we have established a DX strategy story as below and used it as a guide for our DX strategy.

We have broken down the DX strategy into five areas and clearly define what we aim for and key measures for each area. With an understanding of this overall direction that the Group is heading in, we are proceeding with the roadmap, setting defined implementation timelines in the annual business plan taking into consideration each group company’s status and circumstances.

Roadmap for DX

Underlined parts are Key Success Factors (KSF)

| Strategy Category | Vision for end of FY2027※(achievement targets) | Main initiatives |

|---|---|---|

| Digitalization/Innovation in Traditional Banking Business |

|

|

| Improvement of Digital Channels/Expansion of Contact Points with Customers |

|

|

| Strengthening Data Utilization |

|

|

| Enhanced DX Infrastructure |

|

|

| DX Support/Collaboration with Customers and Local Regions |

|

|

※These initiatives are managed on the basis that they will be achieved in three years. However, in the event of significant technological innovations or changes in the environment, revisions may be made in the short term.

Mebuki Financial Group is deploying sustainability initiatives utilizing digital technology from three perspectives: "DX of Group Internal Operations," "DX of Financial Products and Services," and "DX of Client Businesses." We introduce the content of each activity below.

1. Digitalization/Operational Innovation in Traditional Banking Business

To streamline complicated operations attributable to using paper forms or affixing seals, we are taking various measures such as paperless, seal-less, and fax-less measures. Specifically, we first implemented the visualization of operations so that their status can be monitored as data. Then we have been promoting various improvement measures, including implementing digital completion processing, automating operations using RPA, AI-OCR, etc., and driving digital workplace reforms to facilitate the completion of operations without printing out paper copies, beginning with areas that have room for improvement.

At both Joyo Bank and Ashikaga Bank, the utilization of RPA has delivered operational efficiencies through the automation of simple manual tasks, such as device registration, preparation of forms, transcription, validation, and data creation. In order to expand the scope of RPA, the banks are proceeding with the renewal of the RPA system which will help realize a further reduction in working hours in future. With regard to AI-OCR, they are working to expand the number of machine-readable forms, and are further increasing the efficiency of simple data entry work at concentrated back-office departments and some branch offices.

Furthermore, in an effort to innovate sales styles and accumulate customer data to support sales activities, we will overhaul our CRM/SFA infrastructure. In addition, we will also promote the expansion of case studies regarding the utilization of generative AI with a view to achieving further operational efficiency.

Development and utilization of apps for business smartphone

Joyo Bank and Ashikaga Bank have distributed smartphones for business use to bank staff, including part-timers. With the goal of increasing the efficiency of internal operations, the banks are pushing forward with the utilization of their proprietary business apps for operations including over-the-counter operations and sales support.

Currently, Joyo Bank has already developed ten types of business apps. Among these, the Receipt App used in the receipt of items from customers has been particularly well received. The app has been patented as a business model in recognition of its advantages in its UI/UX design, its groundbreaking approach of using a single photo of the received multiple items as evidence, and a function capable of managing information of “when, from whom, to whom, and where the item was received” as digital data using GPS.

Business apps for smartphones

Receipt App

Thoroughly simplified functions

Strategic Utilization of Generative AI in Banking Services

As part of initiatives related to improving the working efficiency of their employees, Joyo Bank and Ashikaga Bank have built an environment where all employees are able to use ChatGPT (Azure OpenAI). By building a closed network, the banks are able to prevent the input data from being used for retraining by OpenAI.

Also, when introducing ChatGPT, all bank staff underwent mandatory e-learning on how to use ChatGPT with a completion test, as part of our efforts to raise employees’ skill level.

Furthermore, in order to expand the use cases for ChatGPT, the banks updated to version GPT-4o in fiscal 2024. In addition, we are steadily increasing the range of functions available, including the making of improvements to prompt templates and adding file upload and RAG※1 functionality.

Screen UI of the generative AI used by Joyo Bank and Ashikaga Bank

2. Strengthening Data Utilization / Expansion of Infrastructure

The Group actively utilizes the data accumulated from the digitalization of internal operations, the apps made available to customers, and their use of our web-based services and other sources. These data are utilized as marketing data to understand each customer more deeply and offer optimized solutions. In addition, we have begun to incorporate these data into our management dashboard to facilitate swift and appropriate decision-making by the Group’s management.

Expansion of data utilization infrastructure

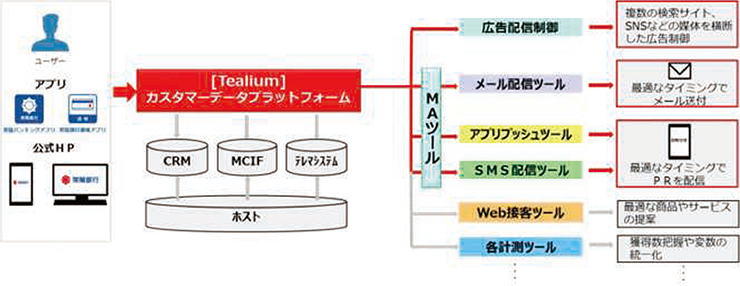

As part of our data utilization infrastructure, we have built an integrated cloud-based data warehouse (DWH)※1 for aggregating internal bank data. In order to utilize the DWH, we have introduced Tableau as a BI tool※2 and Salesforce Marketing Cloud as an MA tool※3. These tools are seamlessly interconnected and together create a unified data infrastructure. In addition, we are expanding the utilization of the Tealium CDP※4, which collects data relating to customers’ internet activities and manages the permissions for such.

The banking app includes a function for disseminating advice to customers. This function allows the banking app to be paired with MA tools, etc., which, in turn, allows for the app to be personalized according to the customer’s attributes and behavior history, helping us to optimize the provision of information and services.

Overview of linking of tools for data utilization

Utilization of statistical AI and machine learning

In the sales division for individual customers, we are working on automating the screening process and optimizing the identification of sales promotion priorities (increasing sales efficiency). Concerning AI adoption in the screening process, AI was introduced in the loan screening process for individual customers (housing and unsecured loans) in December 2023. Previously, screening was an entirely manual process; now, with AI, in approximately 60-70% of all cases, screening results are automatically provided to customers. The ability to respond to screening requests within the same day contributes to the increased attractiveness of our loan products. In addition, we will introduce an AI scoring function in the future so as further improve the judgement accuracy of the AI.

In the sales division for corporate customers, AI-generated lists that predict corporate funding needs are distributed to our branches. This system is operated as Funding Needs AI. This AI uses data on deposits and withdrawals or corporate customers as the main explanatory variables for AI modeling, and by entering the latest data, it will predict their funding needs. At branches, the AI score, the main factors contributing to the score, and examples of action plans created based on the degree to which these factors influence the score are presented. This AI model is utilized primarily among junior staff with less experience.

Also, we have begun using AI-driven statistical processing tools in order to further enhance data analysis operations.

3. Enhanced DX Infrastructure / Development of DX Human Resources

In order to promote DX systematically, it is necessary to renovate system infrastructure and develop human resources. From a medium-term perspective, we are proceeding with the renewal of our core systems and branch systems and shifting on-premises servers to the cloud on a group-wide basis. Further, from a short-term perspective, we are steadily updating each of our individual systems, along with our digital work environment and the devices that we use.

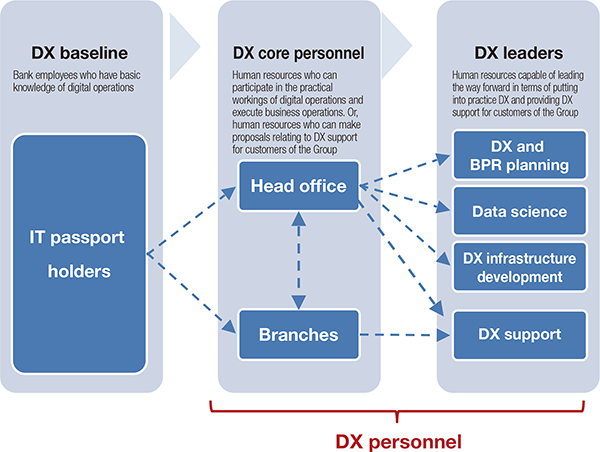

Development of DX human resources suited to actual business conditions and improving the levels of expertise of DX leaders among human resources

We have updated our policy on the development of DX human resources in light of the results of our DX human resources development initiatives set out under the Third Medium-Term Group Business Plan.

We have clarified the objectives we have for the development of our DX leaders by subdividing the objectives into individual “skill categories.” These are then used to set training themes and as a baseline for when designating which employees should be chosen to take part.

Specifically, we reviewed the five digital skill standards※ in light of the actual conditions of the Group, and modified them to four standard skills: DX/BPR planning, data science, DX infrastructure development, and DX support (DX for customers), which is a requisite skill for a regional financial institution.

For details on the results of DX human resources development, please refer here.

※ Guidelines established by the Ministry of Economy, Trade and Industry and IPA to facilitate the acquisition of the basic knowledge, skills, and mindset related to DX by all business persons

Overview of the human resources development system

Training for DX personnel development

Both Joyo Bank and Ashikaga Bank have continued to run the DX Personnel Development Workshop to facilitate the acquisition of the skills required for DX promotion among staff, including design thinking, data analysis, idea creation, and project management.

From 2025, several new training programs will be added, including one on generative AI training, as part of efforts to encourage the skilling up of DX personnel.

Furthermore, by increasing the number of training sessions jointly held by Joyo Bank and Ashikaga Bank, the banks are actively promoting personnel exchanges within the Group.

DX Personnel Development Workshop

Digital Transformation Centered on Strengthening Human Capital

The Group has set forth the democratization of DX in its Fourth Medium-Term Group Business Plan (FY2025–27), promoting an organizational structure that enables all employees of Joyo Bank and Ashikaga Bank to utilize digital technology. For details on the "Roundtable Discussion on Human Capital (Developing DX Personnel)" by those in charge, please see here. (Excerpt from Integrated Report 2025)

1. Improvement of Digital Channels/Expansion of Contact Points with Customers

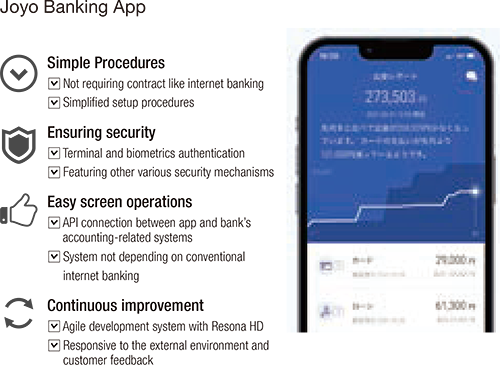

With our banking apps (Joyo Banking App and Ashikaga Bank App) for individual customers, positioned as a core channel, we provide an environment where they can access our banking services conveniently anytime, anywhere.

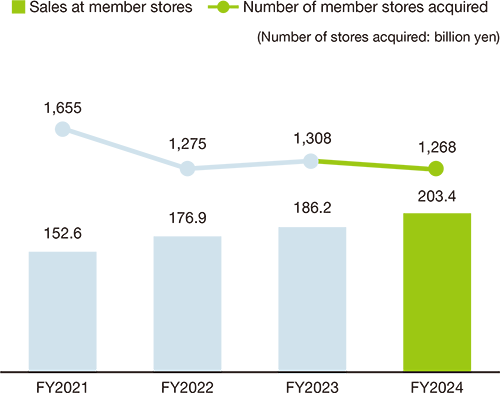

In fiscal 2024, we added new functionality, including for disseminating advice to customers, notifying of scheduled withdrawals, and cancelling scheduled transfers. We also made improvements to the UI for when viewing transaction history. The number of users of the apps now exceeds 1.3 million.

Number of banking app users

Banking App that requires no application or manuals

On the basis of a business alliance with Resona Holdings, Inc. in the digital field, we partially customized the Resona Group’s app to develop our banking apps, which we then began offering in March 2021. We cooperate with Resona Holdings using agile development methods to develop new functionalities for the apps, releasing new features and UI updates approximately every three months. The app’s development included a collaboration with the app design company, teamLab, Inc. The app boasts a speed and level of design not possible for most regional banks to achieves on their own, and provides a level of convenience for customers that negates the need for instruction manuals.

Joyo Banking App

2. Digitalization of over-the-counter operations

In order to digitalize over-the-counter operations, we have introduced the Self-counter Navigation tablets at all our branches and achieved a significant reduction in operational processes by adopting Straight-Through Processing (STP: front-end administrative processing that does not require subsequent processing). In addition, we are working on expanding functionality to make simple transactions such as deposits and withdrawals, bank transfers, and currency exchanges semi-self-service.

We are also promoting cashless payment of various taxes. In June 2024, Joyo Bank received an appreciation award from the Kantoshinetsu Regional Taxation Bureau for our contribution to the promotion of cashless tax payments.

In addition, Joyo Bank and Ashikaga Bank have added a function to 504 of their ATMs (across 154 locations) for reading Local Tax Unified QR Codes, and are working to improve the efficiency of over-the-counter administrative work by allowing tax payments to be made using ATMs.

Daily volume of operational processes (FY average): Hours

3. Cashless & DX Promotion through Regional and Administrative Collaboration Cashless Tax Payment Initiatives

Cashless Tax Payment Initiatives

The majority of payments of national and local taxes are made directly at designated counters at financial institutions, tax offices, and municipalities. The challenge is finding a way to make this more convenient for taxpayers and to reduce social costs associated with the accompanying administrative work. Joyo Bank and Ashikaga Bank are working to spread and promote the use of a greater variety of cashless payment options.

Awareness raising activities by six financial institutions within Ibaraki Prefecture

Joyo Bank, together with Tsukuba Bank, Mito Shinkin Bank, The Yuki Shinkin Bank, The Ibaraki-ken Credit Cooperative, and IBARAKI SHINREN, distributed informational fliers advertising cashless tax payments at the six financial institutions to publicize various cashless payment options to taxpayers, including payment by account transfer or smartphone payment.

This is not limited to just financial institutions; Ibaraki Prefectural Tax Offices, Ibaraki Prefecture, the 44 municipalities within the prefecture, and organizations affiliated with the Ibaraki Prefectural Tax Liaison Council are also working together on an organizational level to promote the use of cashless payments.

Implementation of the “Tochigi Prefecture Joint Promotion Declaration for Cashless Payment of National and Local Taxes”

Ashikaga Bank, together with 32 organizations within Tochigi Prefecture, including local government, financial institutions, and non-government organizations, implemented the “Tochigi Prefecture Joint Promotion Declaration for Cashless Payment of National and Local Taxes.”

In cooperation with 10 financial institutions within Tochigi Prefecture, as well as with Tochigi Prefecture itself and the tax offices of Tochigi Prefecture, Ashikaga Bank is working to further promote the use of cashless options for the payment of taxes and public fees under “All Tochigi.”

Cashless payment of fees for tourism

In Ibaraki Prefecture, there is a cycling course with a total length of about 180 km, including the abandoned tracks of the former Tsukuba Railway and the lakeside road that goes around Kasumigaura Bay. Anyone can rent a bicycle and enjoy the beautiful scenery while cycling, but issues have arisen in introducing cashless payment for the fees.

Joyo Bank, in cooperation with Ibaraki Prefectural Government and Mebuki Card, installed credit card terminals at 10 bicycle rental bases to enable cashless payment.

Introducing cashless payment at local government counters

The introduction of cashless payment at local government counters is being promoted as an important initiative in response to the growing use of cashless payment, particularly among young people. It is also intended to reduce the burden of back-office administrative work related to revenue and to enhance administrative efficiency.

Ashikaga Bank is working to install credit card terminals equipped with POS functions at seven locations, including Sakura City Office and its branch offices, in cooperation with Sakura City of Tochigi Prefecture and Mebuki Card. This enables settlement by credit card, e-money, and QR code.

Cashless payment of application fees by revenue stamp

Mebuki Card is promoting cashless payment for application fees using revenue stamps in cooperation with Tochigi Prefecture. In Tochigi Prefecture, revenue stamps are used to pay fees for approximately 800 types of administrative procedures, including driver’s license renewals. Beginning in October 2024, we initiated a phased transition to a cashless payment system, which is scheduled for completion by FY2025. The prefecture has abolished revenue stamps, which limit the time and location of purchases, and introduced a cashless payment to improve convenience for prefectural residents and improve the efficiency of administrative operations.

Promotion of cashless payment in local regions (Mebuki Card)

1. Digitalization of Regional Business Operations

Initiatives to digitize business-related settlements

Joyo Bank and Ashikaga Bank provide customers with information tailored to their needs--including electronically recorded monetary claims and transfers through Internet Banking--as alternative means of settlement to notes and checks, toward the goal of “completely eliminating the exchange of bills and checks at clearing houses nationwide by the end of FY2026,” as set forth in the “Action Plan of the Growth Strategy” of the Japanese government and the voluntary action plan of the Japanese Bankers Association.

We will contribute to improving the operational efficiency and productivity of regional businesses by promoting the use of these electronic payment methods in local regions.

Provision of information and DX support for growth of regional industries

Joyo Bank addresses regional issues such as chronic labor shortages associated with a declining population by supporting the sustainable growth of regional business operators through productivity enhancement via DX. The bank also holds seminars to present various cases under the latest themes such as cashless payments, compliance with laws and regulations, and operational efficiency through digital technologies.

In addition, Joyo Bank and Ashikaga Bank provide consulting services that identify potential issues for regional businesses taking the first step toward DX and propose future directions.

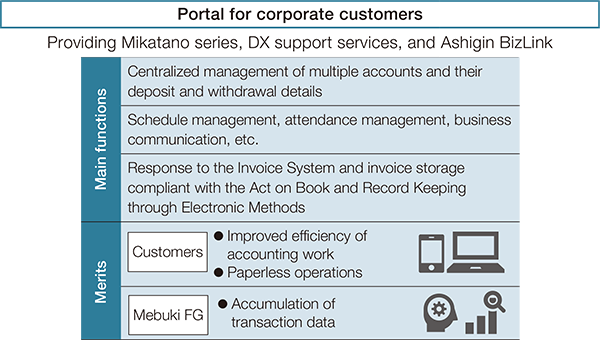

Corporate portal services (Joyo Bank’s Mikatano series and Ashigin BizLink)

We promote the adoption of corporate Internet banking and provide corporate portal services (Joyo Bank’s Mikatano series and Ashigin BizLink) to assist businesses in their cash management and support their efforts to improve the efficiency of their internal operations.

In FY2023, we focused on promoting the use of “densai,” electronically recorded monetary claims, to discontinue the use of traditional bills and notes. In the second half of 2023, Joyo Bank was awarded the Debtor Usage Rate Prize from densai.net Co., Ltd., an organization that manages densai. The prize is provided to financial institutions with a significant increase in customers paying with densai. (The bank was recognized as an excellent bank in this initiative for three consecutive periods.)

Offering “Benefit Support”, Joyo Bank’s welfare program

Benefit Support offers a wide variety of benefits to eligible employees of regional business companies and helps enhance their welfare programs. Eligible employees can access banks’ unique financial products and services, regional perks that help revitalize the regions, and a wide range of perks that can be used nationwide. As options, eligible employees can also attend various types of seminars at discounted prices, such as a financial education seminar and an asset management seminar for employees.

In August 2024, we launched the “Benefit Support” JOYO welfare service app to make the service easier and more convenient to use. Please refer here for details on the app.

2. DX Support/Collaboration with Customers and Local Regions

We offer various seminars to provide various information and introduce our solutions to corporate customers and municipal governments.

Joyo Bank periodically holds online briefing sessions to introduce best DX practices. As of March 2025, a total of 62 sessions have been held, attracting more than 14,000 attendees.

Ashikaga Bank organizes industry-based seminars on themes that match the time as well.

Both Joyo Bank and Ashikaga Bank also provide DX consulting services and escorted support closely following management challenges that individual corporate customers are facing, both of which have been positively received.

Online briefing session introducing best DX practices

Business matching and other cross-industry collaborations, and utilization of external capital

Initiatives for Collaborating with Investees

Joyo Bank is collaborating with Digital Securities Co., Ltd., one of its fund investees, to advance into the field of STO (Security Token Offering) which is a type of fund-raising method using block-chain technology. To date, the bank has provided non-recourse loans to STO funds. Going forward, the bank will continue to offer more STO-related services to meet the diverse fund-raising and asset management needs of our customer companies.

Ashikaga Bank is cooperating with Caters Inc. (in which the bank’s wholly-owned subsidiary, Wing Capital Partners, Ltd., is an investor) and has together established a DX Promotion Project Team to promote DX to customers, drawing on the synergy between the bank’s customer base and Caters’ system development capability. In addition, by leveraging Cater’s expertise, a training program was provided to bank staff to raise their DX customer support abilities.

Working with Customer Companies to Develop Business Apps

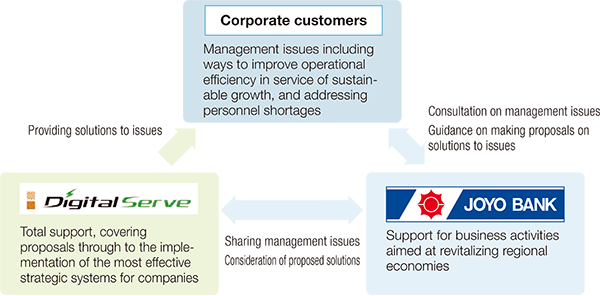

In April 2021, Joyo Bank entered into a business alliance in the IT and digital sector with Digital Serve Co., Ltd., an IT company based in Mito City. Through this alliance, the two companies are working on the joint development of business-use smartphone apps and on providing support for customer companies and local communities on the DX transition. They have already developed ten types of business app, including the Receipt App, which are in daily use in banking operations.

In addition, Joyo Bank leverages the technical capabilities and abundant experience of Digital Serve to help find DX-driven solutions to the various issues faced by the customer companies of Joyo Bank.

Ashikaga Bank has also introduced a company-vehicle app※1 and a sales support app※2, and is working to streamline operations.

Business alliance scheme of “Promoting and Supporting the Implementation of DX for Customers and Local Regions”